China Office Market Overview

Sunny Zhang,

MRICS

Director, BOMA China

Director, Cushman & Wakefield China

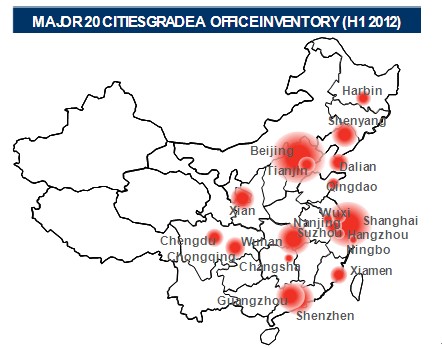

The current stock of Grade A office buildings are predominantly located in 1st-tier cities. As of Q2 2012, the total inventory of Grade A office supply in the major 20 cities reached 30 million square meters. Beijing, Shanghai, Guangzhou and Shenzhen accounted for 62% of the total inventory, or over 18.83 million square meters. Beijing with 7.91 million square meters of Grade A (including Prime offices) office inventory ranked at the top of the country.

Reflecting the high volume of development activity, Chinese cities took 23 of 25 slots in Cushman and Wakefield’s 2011 Global Land Transaction Ranking. As a result of a series of tightening monetary policies towards housing purchases, development has shifted towards the commercial sector. However, the prevalence of strata-titled developments as well as a lack of high-quality projects represents notable weaknesses in some 2nd-tier cities. Additionally high volumes of future supply coupled with insufficient industry demand are likely to contribute to softening rents and upward pressure on vacancy rates.

Source: Cushman & Wakefield Research

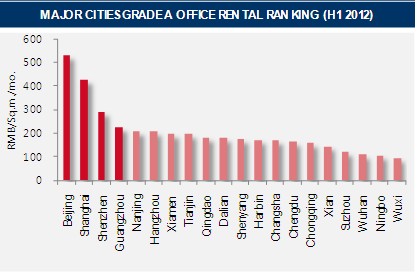

Beijing office rents lead the country. Growth in Grade A office rents eased as demand moderated in major markets. Grade A office rents rose across all our selected cities in China, but quarterly increases varied in major markets. Beijing, as the most expensive office market in China, just behind Hong Kong and Tokyo, ranked third in Asia Pacific. After heady growth last year, Beijing’s Grade A office rents are now cooling off. In Q2 Shanghai’s office rent’s displayed a modest rise in rent, after experiencing two consecutive quarters of flat growth. Owing to the sluggish economy and falling foreign demand, Guangzhou and Shenzhen’s office rents remained stable. However, with the maturing of emerging markets and increasing urbanization, rents in emerging markets have steadily increased in cities that C&W tracks. Office rents in the Nanjing, Hangzhou and Xiamen markets have seen stable growth and led the pack of 2nd tier cities.

Source: Cushman & Wakefield Research

Note: Rental rate refers to Net Effective Rent is calculated based on net floor area.

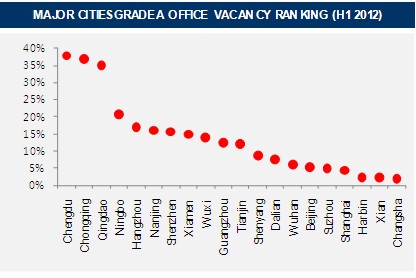

Vacancy in a number of 2nd tier cities office market remain high. Moderate demand continued to chip away at Grade A vacancies in most markets. Major cities such as Shanghai, Guangzhou and Shenzhen have witnessed a further decline in vacancy rates over the first half of 2012. To some extent, new supply in non-core areas of Beijing has absorbed some of the excess demand, alleviating the competition from years of tight supply in the CBD. Landlords in major cities are upgrading their tenant mix by offering more attractive rents and better terms to tenants in order to improve building image and profile. Nationwide, Grade A office markets in 1st-tier cities are still the first choice for multinational corporations, and the demand for offices has shown a steep upward tendency. Despite the considerable amount of office stock in Beijing and Shanghai, vacancy rate remains low due to limited available space. For Guangzhou and Shenzhen, even with a large future supply, the market remains active, and the net absorption rate has been high. Among the 2nd-tier cities that C&W tracks, development activity remains focused on commercial office, while demand for office buildings in Tianjin and Chengdu remain high. Vacancy rates for Chengdu, Chongqing and Qingdao were highest among the major twenty cities due to large amounts of Grade A office entering the market. Vacancy rates were low in 2nd tier cities such as Changsha, Xi’an, Harbin and Suzhou, despite less availability of higher quality Grade A stock. The lack of Grade A offices that multinational corporate tenants desire is a potential opportunity for future development projects.

Source: Cushman & Wakefield Research

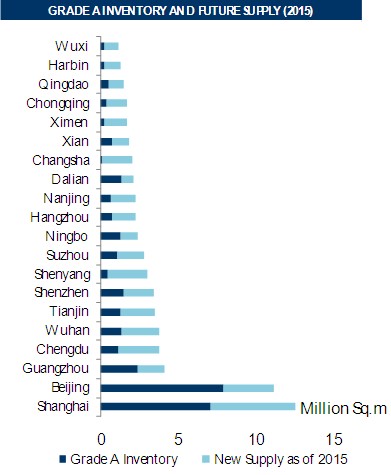

Future development remains robust in major markets. Based on 20 cities that C&W tracks, the office pipeline shows over construction of over 37.61 million square meters of new projects that will deliver through 2015. Development activity is particularly strong in Shanghai and Beijing with over 5.43 and 3.21 million square meters of future supply, respectively. Among 2nd tier cities, Tianjin, Chengdu, Wuhan and Shenyang will see as much as 2 million square meters of new supply enter their markets respectively in the next two years, as well as see their total office inventory double.

Source: Cushman & Wakefield Research

Demand continues to be brisk in major markets. As of H1 2012, domestic companies accounted for 57% of total transactions, a 21 percentage point increase compared to the same period last year. Shanghai’s market demand is still dominated by MNCs. However, demand from domestic companies shows an increasing trend in overall transactions. In other major cities, domestic companies and local SMEs are still the main sources that drive office demand. MNC, or MNC subsidiary expansions, represent a relatively small proportion of demand in these markets. With regards to office demand, the finance and IT industries are still the predominant growth drivers. In Beijing, the high-tech, finance and cultural and creative industries generated robust demand for office; in Shanghai, the finance and pharmaceutical industries are two major driving forces. On the other hand, geographic variations exist in the energy and pharmaceutical industries as well as professional services. Xiamen, Ningbo, Shenzhen, all coastal cities in southeast China, benefit from an export-oriented economy, trade, logistics and related, specialized services, which all create healthy demand for offices. Compared to mid-west region represented by cities such as Wuhan, Chengdu and Xi’an, excellent infrastructure and abundant educational institutions help make them the best options for pharmaceutical, high-tech and cultural and creative industries to establish offices.